Serving Up Safety: The Food Truck’s Guide to Summer Festival Liability in Central MA

Summer in Central Massachusetts is the ultimate season for mobile eateries. From the massive crowds at the Worcester Food Truck & Craft Beverage Festival on the Common to the Wachusett Mountain Summer Food Truck Fest and local pop-ups across Auburn and Gardner, the opportunities to park, cook, and profit are endless.

But before you fire up the grill and start serving those lobster rolls and empanadas, there is a hurdle you have to clear: the festival organizer’s vendor contract.

Organizers of large-scale summer events don't just ask you to bring great food; they require you to bring bulletproof insurance. If you are assuming your basic business setup covers everything that happens at a weekend festival, you might be leaving your business exposed.

Here is exactly what you need to know about vendor liability, event requirements, and keeping your food truck protected this summer.

Full-Time vs. Part-Time: What Policy Do You Actually Need?

When you sign a vendor agreement for a Central MA event, the organizers (and often the city itself) are transferring the risk of your operation squarely onto your shoulders. How you cover that risk depends on your business model:

For Full-Time Trucks: If you operate year-round (or close to it), your standard annual General Liability (GL) and Commercial Auto policies should cover you wherever you park. You usually just need to prove to the festival that this policy exists and meets their limits.

For Part-Time Pop-Ups: If you only operate a tent or trailer a few weekends a summer and don't carry an annual policy, you will need to purchase a standalone Special Event Policy. This covers you specifically for the 1-to-3 days of the festival, handling bodily injury and property damage that occurs within your footprint.

Decoding the Festival Contract

When you read through the vendor application, you will likely see a few insurance terms repeated. Here is the plain-English translation of what they actually mean.

The Certificate of Insurance (COI)

This is your golden ticket. A COI is simply a one-page document from your insurance agent proving you have active coverage. You cannot just say you are insured; you have to submit this form before you are allowed to load in.

"Additional Insured" Status

Almost every festival requires you to list them as an "Additional Insured" on your policy. For example, if you are serving at Elm Park, the City of Worcester will want to be named. This means if a customer sues the city because they got food poisoning from your truck, your insurance will step in to defend the city.

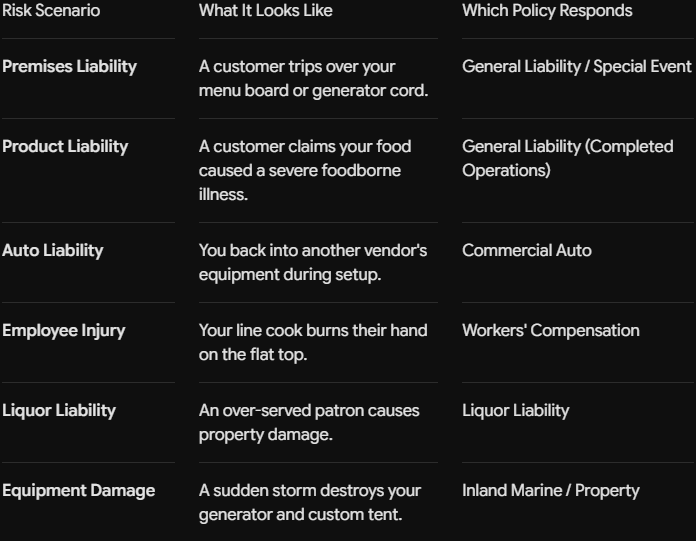

Navigating the Big Festival Risks

Festivals are chaotic, crowded, and fast-paced. Here is how your coverage breaks down across the most common claims.

A Table looking at Festival Risk Scenarios, What they look like, and which Insurance Policy responds.

Your Pre-Festival Checklist

Before you pay your vendor fee and order your ingredients for your next local festival, take these five steps:

Read the Insurance Limits First: Most municipalities and large organizers require at least $1,000,000 per occurrence and a $2,000,000 aggregate limit for General Liability. Ensure your policy meets the threshold.

Don't Forget Your Staff (Workers' Comp): If you are bringing W-2 employees to help sling food, the city or organizer will almost certainly demand proof of Workers' Compensation on your COI. (1099 contractors are a different story, but employees must be covered).

Check Your Beverage Menu (Liquor Liability): Pouring craft beer or mixing margaritas? Standard General Liability explicitly excludes alcohol-related claims. You must secure standalone Liquor Liability coverage.

Check Your Permits & Inspections: Your insurance is generally only valid if you are operating legally. Ensure your fire extinguishers are tagged, Board of Health permits are current, and propane setups meet local fire codes.

Call Your Agent Two Weeks Out: Do not wait until the Friday before a Saturday festival to request a COI with an Additional Insured endorsement. Give your insurance agent time to review the contract and issue the paperwork.

You focus on the menu and the summer crowds; let your insurance handle the what-ifs. If you need help reviewing a festival contract or securing a COI for your food truck, reach out to our team today to make sure you are covered.

- John Suprenant

Owner/Principle